Credit Bureau of Canada: An In-Depth Guide

The Credit Bureau of Canada plays a crucial role in the financial landscape of the country, impacting individuals, businesses, and lenders alike.

Understanding how these bureaus function, what information they collect, and how they influence your financial life is essential for making informed financial decisions.

This article provides a detailed overview of the Credit Bureau of Canada, its operations, and its significance.

What is a Credit Bureau?

A credit bureau, also known as a credit reporting agency, is an organization that collects and maintains individual and business credit information.

In Canada, the two primary credit bureaus are Equifax and TransUnion. These bureaus gather data from various sources, including banks, credit card companies, and other financial institutions, to create credit reports and scores.

Credit bureaus do not make lending decisions; instead, they provide the information that lenders use to assess the creditworthiness of an individual or business.

This information is critical in determining whether someone qualifies for a loan, the interest rate they may receive, and even the credit limits on their credit cards.

→ SEE ALSO: Understanding Childhood Trauma and Its Impact on Adults

How Does the Credit Bureau of Canada Work?

The Credit Bureau of Canada operates by collecting data from a wide range of sources. This data includes information on loans, credit cards, mortgages, payment histories, and any defaults or bankruptcies.

The information is then compiled into a credit report, which is updated regularly as new data becomes available.

Each credit bureau operates independently, meaning that your credit report may vary slightly between Equifax and TransUnion. However, the general information contained in your reports will be similar.

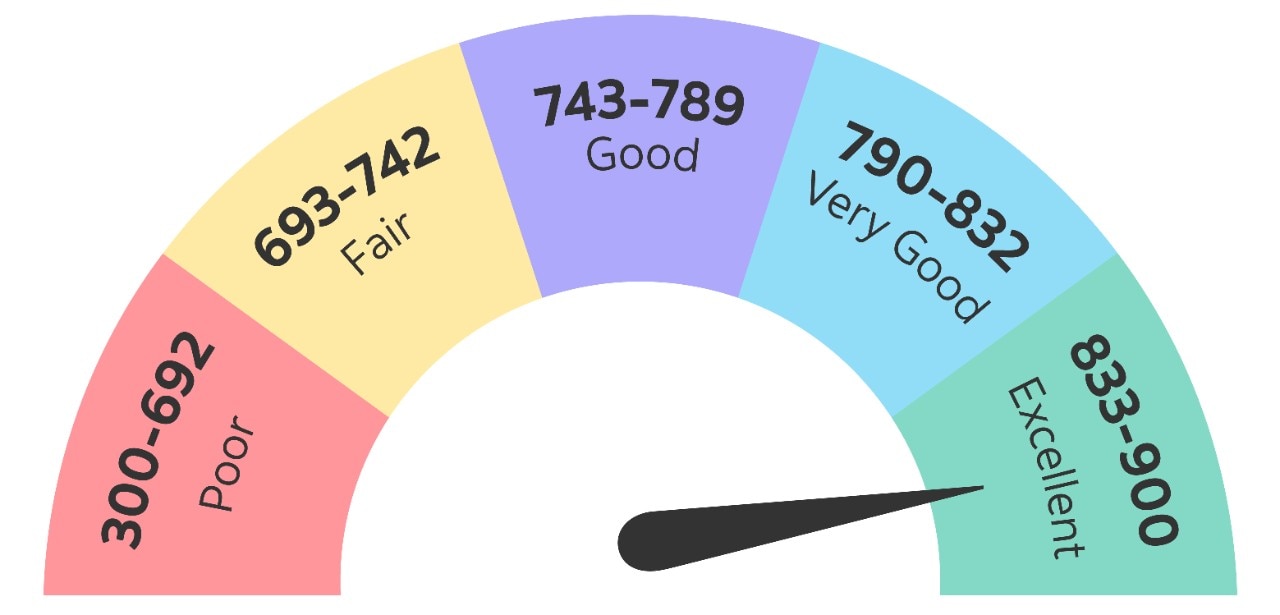

The credit bureaus assign a credit score based on the data in your credit report, typically ranging from 300 to 900. This score is a numerical representation of your creditworthiness, with higher scores indicating better credit.

Importance of Credit Scores

Your credit score is one of the most important factors in your financial life. Lenders, landlords, and even some employers use credit scores to make decisions about you.

A good credit score can open doors to lower interest rates on loans, higher credit limits, and better financial opportunities.

Conversely, a poor credit score can make it challenging to obtain credit, and when credit is available, it often comes with higher interest rates.

In Canada, a score above 760 is generally considered excellent, while scores between 700 and 759 are considered good. Scores below 650 may make it difficult to qualify for prime loans and may result in higher interest rates.

How to Access Your Credit Report

In Canada, individuals have the right to access their credit reports from both Equifax and TransUnion for free once a year.

This access is crucial for monitoring your credit history and ensuring that the information in your report is accurate.

Errors on your credit report can negatively impact your credit score, so it’s important to review your report regularly and dispute any inaccuracies.

You can request your free credit report by mail or online through the websites of Equifax and TransUnion.

Additionally, both bureaus offer paid services that provide more frequent access to your credit report and score, along with credit monitoring services that alert you to significant changes in your credit profile.

The Impact of Credit Bureaus on Financial Decisions

Credit bureaus play a pivotal role in the financial decisions made by both individuals and lenders. For individuals, understanding their credit report and score is essential for managing their financial health.

For lenders, credit reports provide a comprehensive view of an applicant’s credit history, helping them assess the risk of lending money.

A strong credit history can lead to better loan terms, such as lower interest rates and more favorable repayment conditions. On the other hand, a poor credit history can limit access to credit and increase the cost of borrowing.

This makes it essential for individuals to manage their credit responsibly, paying bills on time, keeping credit card balances low, and avoiding excessive applications for new credit.

How to Improve Your Credit Score

Improving your credit score is possible with discipline and time. Here are some strategies to boost your score:

- Pay Your Bills on Time: Late payments can significantly harm your credit score. Setting up automatic payments or reminders can help ensure that bills are paid promptly.

- Keep Credit Card Balances Low: High credit card balances relative to your credit limit can negatively impact your score. Aim to keep your balances below 30% of your credit limit.

- Avoid Unnecessary Credit Inquiries: Each time you apply for credit, a hard inquiry is recorded on your credit report, which can slightly lower your score. Avoid applying for unnecessary credit.

- Check Your Credit Report for Errors: Regularly review your credit report to ensure that all information is accurate. Dispute any errors with the credit bureau to have them corrected.

- Consider a Secured Credit Card: If you have a low credit score or no credit history, a secured credit card can help you build credit. With a secured card, you provide a deposit as collateral, and your payment history is reported to the credit bureaus.

- Diversify Your Credit Mix: Having a mix of credit types, such as a credit card, mortgage, and installment loan, can positively impact your score. However, only take on credit you can manage responsibly.

Credit Monitoring and Identity Theft Protection

Given the importance of your credit score, many people opt for credit monitoring services. These services track changes to your credit report and alert you to any suspicious activity, which can be a sign of identity theft.

Identity theft is a growing concern, and monitoring your credit can help you detect and respond to it quickly.

Both Equifax and TransUnion offer credit monitoring services, which include regular access to your credit report and score, as well as alerts for any significant changes. Some financial institutions also offer credit monitoring as part of their services to customers.

Conclusion

The Credit Bureau of Canada plays an integral role in the country’s financial system.

Understanding how credit bureaus work, what factors influence your credit score, and how to maintain a healthy credit profile is essential for anyone looking to manage their finances effectively.

By staying informed and proactive about your credit, you can make better financial decisions and improve your overall financial health.

Whether you’re applying for a mortgage, renting an apartment, or securing a job, your credit report and score will be a key consideration.

→ SEE ALSO: What is Mortgage Refinancing?

Beatriz

Beatriz Johnson is a seasoned financial analyst and writer with a passion for simplifying the complexities of economics and finance. With over a decade of experience in the industry, she specializes in topics like personal finance, investment strategies, and global economic trends. Through her work, Beatriz empowers readers to make informed financial decisions and stay ahead in the ever-changing economic landscape.